It’s fair to say the last 12 months have been extraordinary from an MIBI perspective. Never before has the Bureau had to deal with issues of such geopolitical magnitude, all undertaken while maintaining our regular service and also seeing through the rollout of important new measures which will themselves have a significant impact on the industry.

In the face of these major developments, people would be forgiven for forgetting about the day to day mandate of the MIBI – but we most certainly haven’t. Our raison d’etre has always been to ensure the victims of accidents caused by uninsured and untraced vehicles are fairly and efficiently compensated.

During 2018, that meant assisting 3,589 claimants through the provision of a payment from the MIBI, a 4% increase on the previous year. We also settled a total of 3,996 claims.

This involved a total payout of €77 million in net claims payments. This figure marked a 23% increase on the 2017 figure, driven primarily by a large number of claims which came to more than €1 million. The MIBI has also implemented a new preferred – but not mandatory – Periodic Payment Order (PPO) strategy in readiness for their use. We believe this model is the fairest compensation mechanism available for catastrophically injured accident victims and we hope to see this provision utilised for claims of this nature in the future.

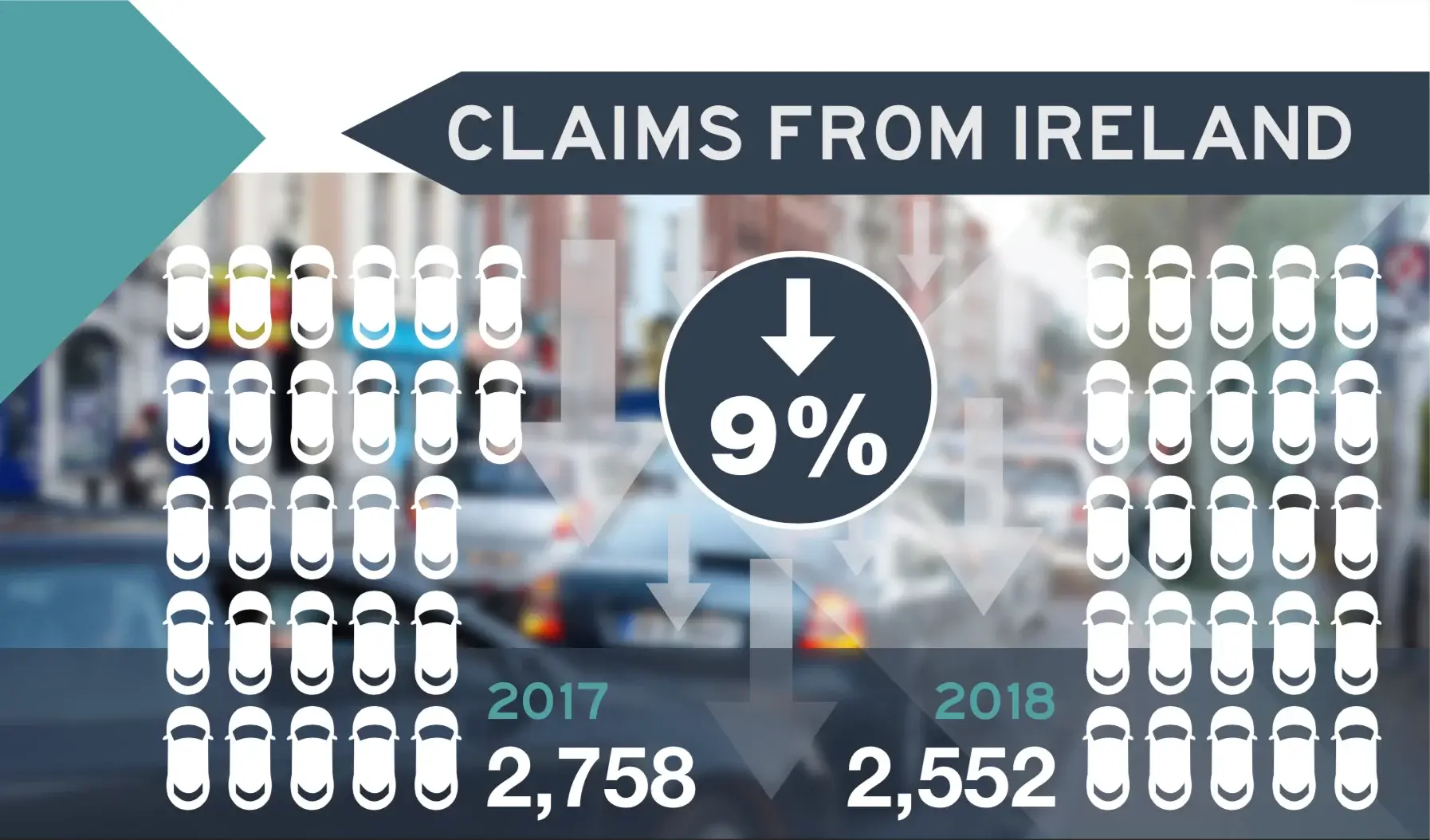

The claim notifications we received for uninsured and untraced accidents dropped in 2018, with a 9% reduction from 2017. This is a level which would seem to have been maintained so far in 2019.

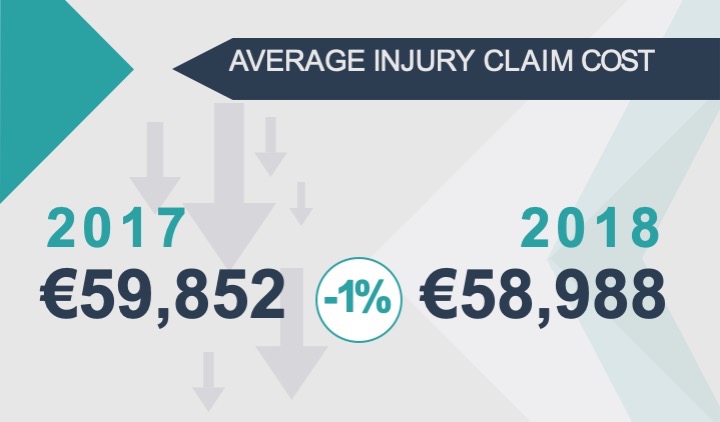

The average injury claims cost also dropped slightly, falling to just under €59,000 in 2018. However that remains at a very high level.

The largest single payout in 2018 was more than €3.4 million, which arose from an accident that unfortunately involved a life altering injury.

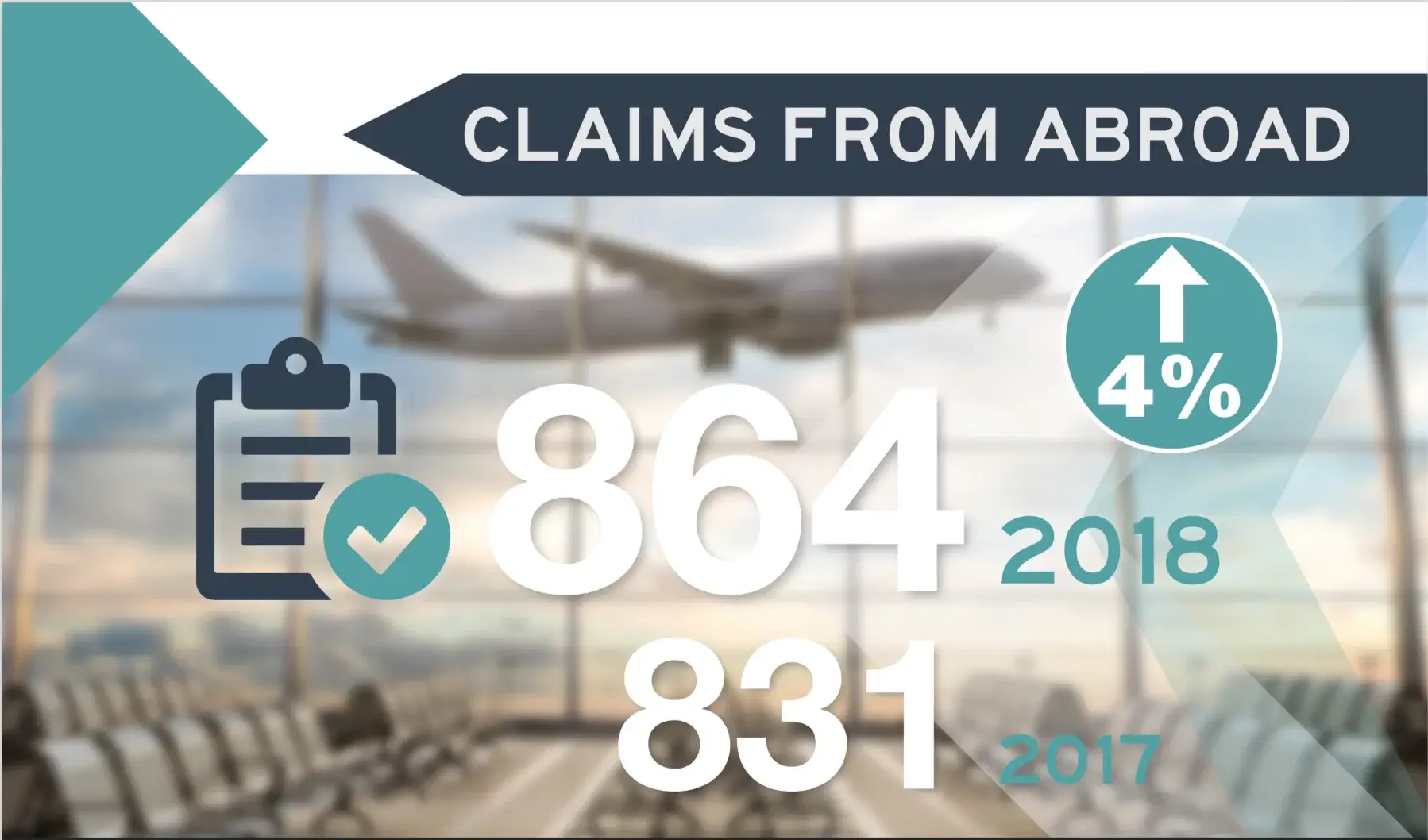

The MIBI’s responsibilities of course extend beyond accidents which take place in Ireland. Under the Green Card system the MIBI is ultimately responsible for claims from accidents caused by Irish registered vehicles visiting other countries. If we are unable to find an insurer, these claims are handled by the relevant foreign bureau and then the MIBI will reimburse that bureau for the claim in question.

There was a 4% increase year on year for these claims from abroad in 2018.

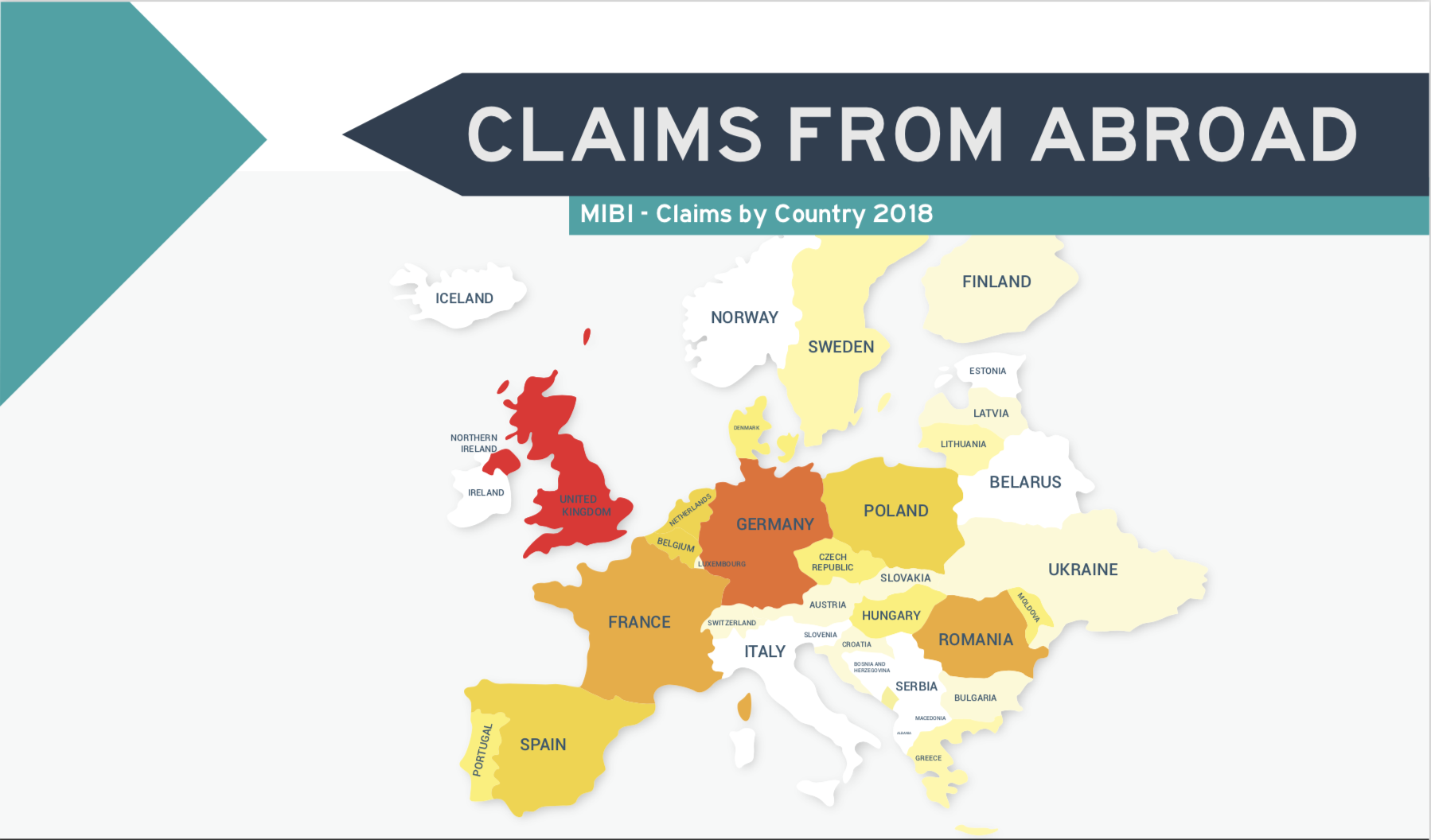

This rise mainly arose from an increase in accidents in the UK (up 19 claims) and Romania (up 10 claims). As this heat map shows, the vast majority of the foreign claims came from the UK (574). Germany came next (68 claims), then France (42 claims) and Romania (37 claims).

One of the key developments over the past 12 months has been the introduction of the Motor Insurers’ Insolvency Compensation Fund (MIICF). The MIBI is playing a key role in the management of this fund, which effectively will act as a ‘rainy day fund’ to protect against motor insurance insolvencies like those seen in the cases of Setanta and Enterprise Insurance.

This fund allows for payments made under the Insurance Compensation Fund (ICF) to rise from 65% of the total claim, to 100%. The Central Bank has taken over the management of the ICF, while the MIBI has established and is administering an Ex Ante Industry Fund – i.e. the MIICF. If required the Central Bank, through the ICF, can then call on the MIICF to provide the ‘35% share’ of compensation due to claimants of the insolvent motor insurance company.

The MIICF began collecting the first tranche of payments in June of this year. This followed a deferred start negotiated with Government, to allow the motor insurance providers time to prepare for this new requirement and to update their processes and systems accordingly.

Over time the fund is expected to collect €200 million, at which point the contributions from the motor insurance companies operating in the state will be capped.

Of course, the issue which has certainly received the most public attention this year has been the potential requirement for Green Cards.

As most people will be familiar with, at the beginning of 2019, the MIBI warned that should the UK leave the European Union without a deal, then a Green Card would be required for any Irish registered vehicle driven in the UK, including Northern Ireland. This followed extensive, wide ranging discussions with the industry, the Irish Government, our peer bureaus across Europe and our colleagues in the UK.

With Brexit originally scheduled for 29th March, ensuring those who may need a Green Card would receive one on time involved a massive logistical operation both from the MIBI as well as the motor insurance companies and brokers operating in this country.

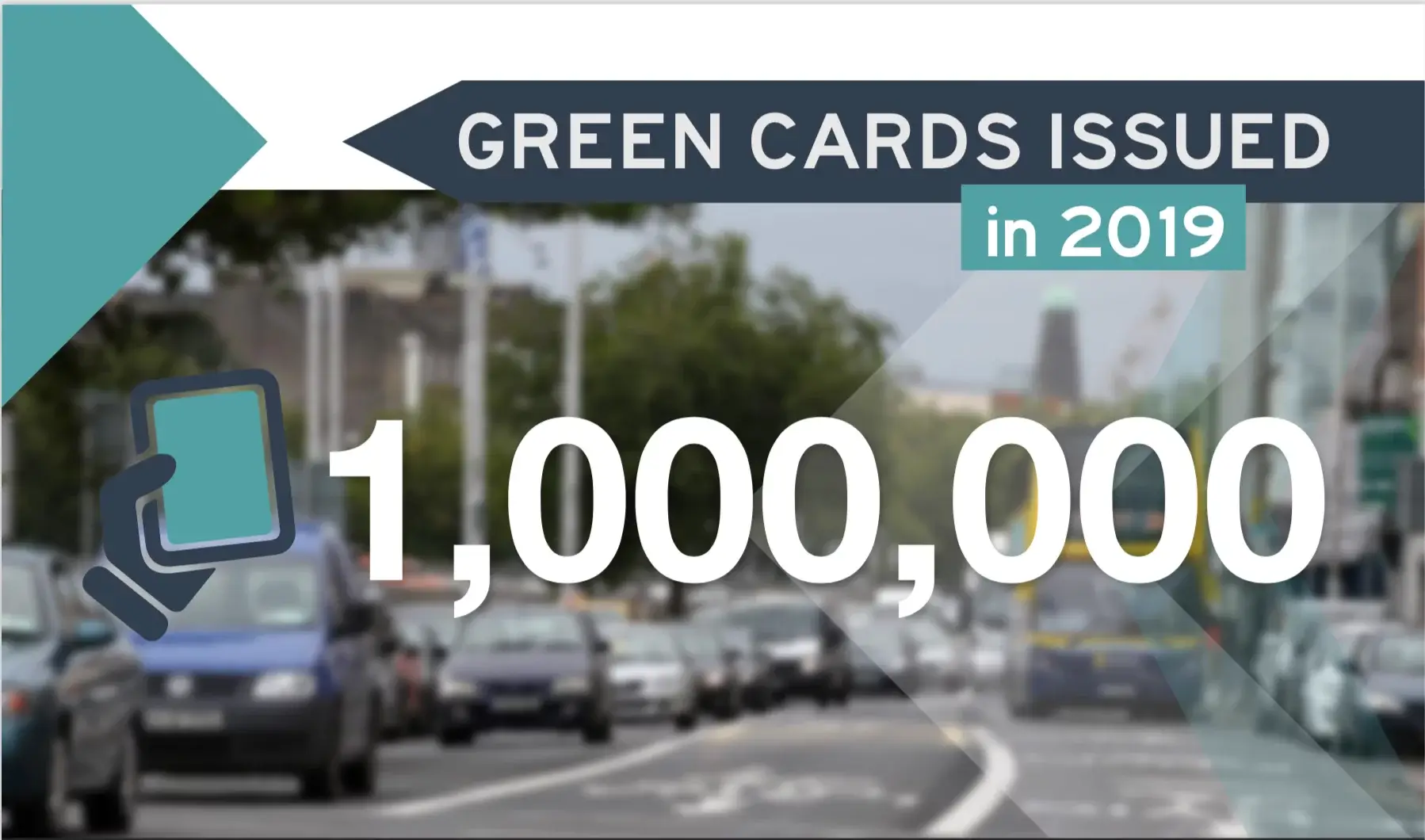

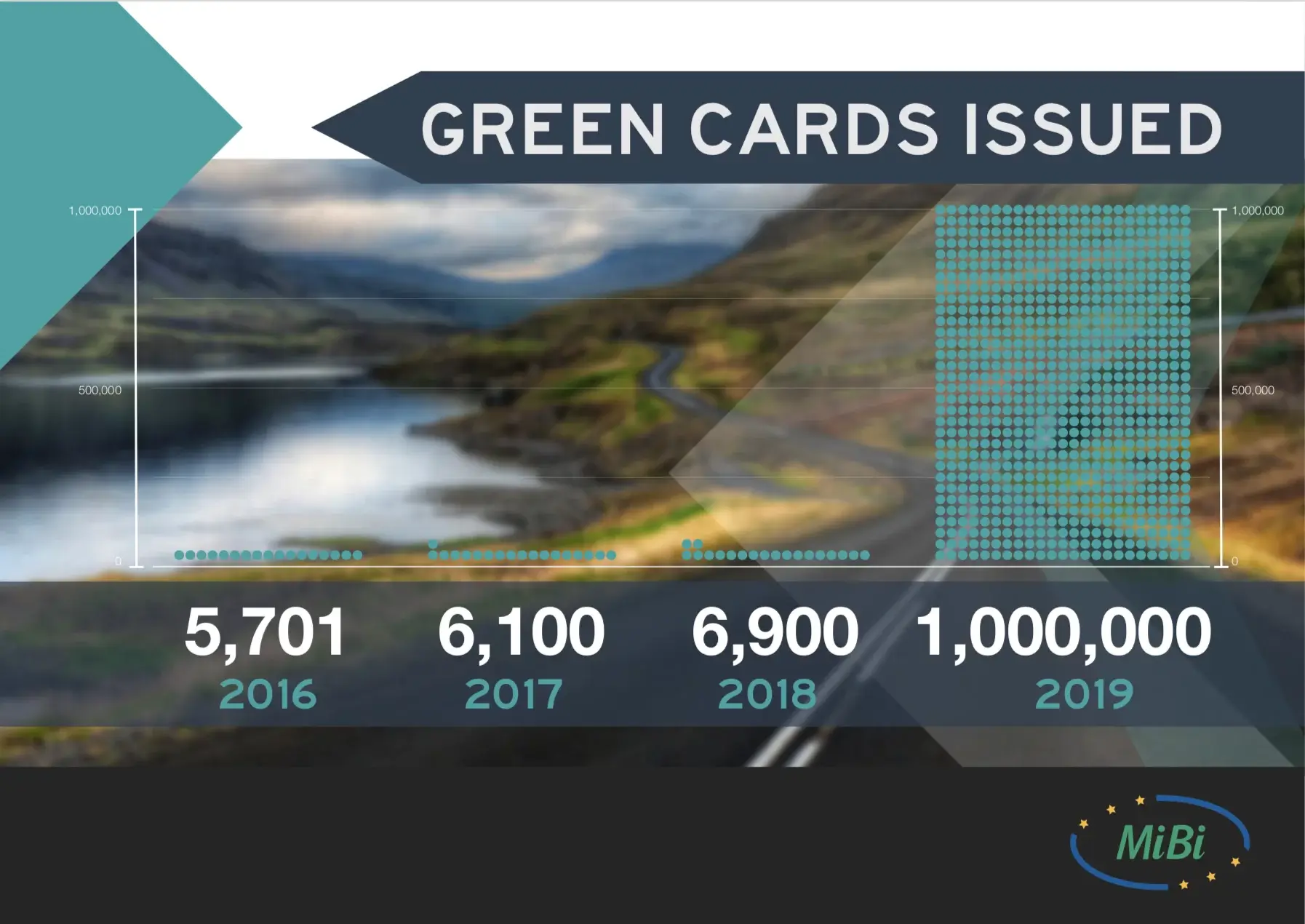

In total the MIBI provided a total of 1 million Green Cards to insurance companies and brokers for provision to their policyholders. These were hard copy documents, with electronic templates also issued.

To put the logistics in context, this was almost 145 times as many Green Cards as we had issued in 2018.

The scale was massive and it was something that neither the MIBI nor the rest of the motor insurance industry in this country has ever undertaken before. For example if these hard copy green cards were to be put end to end, they are as long as 3,900 747 Jumbo Jets…

Or they could cross from Dublin to Holyhead in Wales 2.5 times.

Of course, we didn’t just need to distribute the Green Cards to the motor insurance providers – we also had to ensure the public at large was aware of this issue and the need to possess a Green Card if there was a ‘no deal’ Brexit. The MIBI undertook extensive communications activity which saw the message carried throughout the Irish news media and featuring on TV, radio and throughout the national and regional press. We also provided extensive briefings to the Government, Members of the Oireachtas and other key policy stakeholders on this matter.

An unprecedented public awareness campaign was also undertaken by the MIBI, which was aimed at making sure that every motorist in the country was aware of the possible requirement for Green Cards. This campaign reached an estimated total of 7.1 million radio listeners and also received over 2 million digital impressions.

Thankfully the story didn’t end there. After the Brexit deadline was extended to its current schedule (i.e. 31st October 2019), the MIBI continued its outreach to the UK Government on whether there were means of mitigating against this onerous requirement which was going to cause bureaucratic difficulties for Irish motorist, British law enforcement authorities and the insurance sector alike.

In August of this year, following months of delicate discussions and legislative clarifications, the UK Department of Transport was able to confirm to the MIBI that Green Cards would no longer be required if there is a ‘no deal’ Brexit. A much more streamlined and straightforward process is now in place, with Irish registered vehicles only needing a valid insurance disc as proof of insurance for law enforcement authorities in the UK, including Northern Ireland.

Unfortunately this provision can’t be reciprocated until such time as action is taken by the European Commission under the EU Motor Insurance Directive, to allow the UK to be recognised as a ‘third country’ that can join the green free circulation zone. Ireland is subject to the collective position, as a continuing member of the EU. This means that UK registered vehicles will still require a Green Card when travelling to Ireland (as well as all other EU countries) – if there is a ‘no deal’ Brexit. We have been pressing the European Commission to amend the directive to address this issue and we will continue to work with the Irish Government and the Council of Bureaux to press this case.

This is just a short synopsis of what has been a 12 months like none before for the MIBI. There are a wide range of additional activities – beyond those mentioned in this piece – which we have been undertaken over the last year. For example, our strong progress in fraud prevention and debt recovery. These two subjects will covered in further pieces to be published shortly.

While it has been a year full of major activity, the work of the MIBI continues as always and we hope and expect to have further major announcements to share in the year ahead, including developments around the Motor Third Party Liability (MTPL) and Automatic Number Plate Recognition (ANPR) project, the implementation of the PPOs and the move towards enhanced data analysis and decision making. In their own right each of these hold the potential for further unparalleled impact and we are excited about how they will benefit the work of the MIBI over the next 12 months.